How to Invest in Your 20s

- Why the Recent Rise in Stock Buybacks Is a Good Sign for Investors

- AI 'Outperforms' Human Financial Analysts, According to New Research

- Here's Why Crypto Prices Are Jumping This Week — and What's Next

- Meme Stock Flop: GameStop Investors Lost Over $13 Billion Last Week

- GameStop and Meme Stock Mania Are Back. Should You Join?

- Coinbase's New Direct Deposit Feature Will Let You Get Paid in Crypto

- All the Big Grocery Stores and Fast Food Chains With Special Deals This Summer

- Why States With No Income Tax Aren't as Affordable as They Seem

- Only 1 in 5 People Think College Is Worth the Money if You Need Student Loans

- 4 Best Extended Car Warranties of 2024

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

It’s understandable why many young people don’t invest: They’d rather use their money elsewhere, or they might not think they have any extra cash available for investing.

But investing in your 20s is a golden opportunity to build wealth, especially if you embrace the right level of risk with the understanding that time is on your side.

Last month, former financial professional and current personal finance personality Mark Palmer posted on X (formerly Twitter), "If I was 20 years old right now, here is what I'd be investing in ..." The post received nearly 160,000 views, but more importantly, it reignited the conversation about how and why young people should be investing — and how and why their portfolio allocations should be different than older generations.

Palmer's list of theoretical investments included some high-risk propositions, such as putting 10% into bitcoin and another 10% in individual stocks that he has "a lot of conviction in," along with larger chunks in exchange-traded funds (ETFs). He acknowledged that "everyone is different," and "what works for me may not work for you."

Regardless of whether you agree with his specific selections, the general thesis is one worth considering, especially if you're young: Diversify, focus on growth investments, and don't shy away from risk.

Young investors: Higher risk is OK

Greater risk can result in greater reward. But it can also contribute to greater losses, at least in the short term. That's why conventional wisdom says investors should begin adjusting their holdings as they approach retirement to reduce risk exposure and protect capital with more conservative assets like CDs and Treasury bonds.

However, for 20-somethings, the opposite holds true. That cohort should be embracing "risk-on" strategies as their investment timelines permit more room for more recovery. That means embracing higher risk asset classes like stocks as opposed to safety-oriented assets like bonds. Going a step further, it also implies focusing on growth stocks versus value stocks. Whereas the latter are often steady, reliable dividend-paying assets, the former routinely see more upside potential.

According to Bill Van Sant, a certified financial planner who is executive vice president and managing director at Girard, a Univest Wealth Division, younger investors' risk tolerance should be much higher, whether that means individual stocks or funds slanted towards aggressive growth. "You simply pick a growth fund, 100% equities, stock. There's no looking at bonds or fixed income at that age."

Gen Z is already demonstrating a propensity for higher risk assets. Data from online investment platform Saxo shows that among young investors, 60% own stocks and 54% own crypto.

The more diversified approach is to put money in ETFs with broad exposure to large-cap growth companies. The Schwab US Large-Cap Growth ETF, for example, provides access to Microsoft, Apple, Nvidia, Amazon, Meta, Alphabet, Eli Lilly and Broadcom all in one fund with a low expense ratio and without having to own each stock individually.

As for those expense ratios or management fees, Van Sant says, "Investors should pay attention to expenses, but don't let that completely consume or derail the investment ... Focus on your real return after taxes and inflation."

When factoring for real returns, the growth potential of a portfolio composed of equities (stocks, ETFs and mutual funds) can perform better for a younger investor than traditional, conservative portfolio allocations like the 70/30 or 60/40 models, which are split between equities and fixed income assets like CDs and bonds.

Start investing for retirement now

A January 2024 poll conducted by Northwestern Mutual found that Americans now believe they'll need $1.46 million to have a comfortable retirement. The problem, however, is 50% of women and 47% of men between the ages of 55 and 66 have no retirement savings at all, according to U.S. Census Bureau data.

Van Sant says that getting started on a path to retirement now is the key to being prepared later, even if it's the only investing 20-somethings can commit to.

"The number one thing to do is enroll in a retirement plan. The majority of employers have them now, and you start at 10% [contribution]. Your budget will adapt," he says. "Trust the process. Retirement savings is a marathon, not a sprint."

One the biggest advantages of participating in a defined contribution plan like a 401(k) is gaining access to an employer's match, which is akin to free money. Like employee contributions, an employer match is money added on a pre-tax basis. On average, companies will match dollar for dollar contributions from 4% to 6% of a worker's pre-tax compensation, up to a certain amount.

If you're unable to devote 10% of your salary out of the gate to a retirement plan, try to at least put aside the maximum employer match amount to get the ball rolling.

Van Sant also stresses the importance of increasing contributions when it's financially feasible. "Give yourself a retirement raise each year when your pay increases or when you can afford it," he suggests, even "if that's only a 1% increase" from your current contribution.

For those who don't have access to an employer-sponsored plan, a tax-advantaged Roth IRA or self-employed retirement plan can be equally effective. The important part is just getting started. Van Sant says younger generations are showing signs of being "more saving-conscious" partly because they're aware of what can go wrong if they're not prepared for retirement.

"You see grandparents going back to work now. That resonates. The biggest challenge to retirees is longevity risk," says Van Sant. "The younger generation has more appreciation for that."

Embrace the power of compound interest

While older Americans are fretting about how far their money will stretch in retirement, many members of Gen Z — those born between 1997 and 2012 — are preoccupied with figuring out their career paths and whether or not they'll ever be able to afford a home.

Despite data showing younger generations doing a better job with saving for retirement and investing compared to older generations when they were the same age, the average age for people today to begin investing is 34 years old, according to the Financial Times. That means Gen Z could be doing more as a whole while embracing strategies that make sense given their age.

Compound interest can have an incredible effect on investments, but getting started early is critical. The average investor getting their start at age 34 is missing out on a decade or more of compounding that would otherwise have an outsized impact on their portfolio's growth.

"If you started 10 years earlier when you're 24," says Van Sant, "you don't have to put in nearly as much to get to the same end-dollar goal ... the later your start, the more you have to play catch-up."

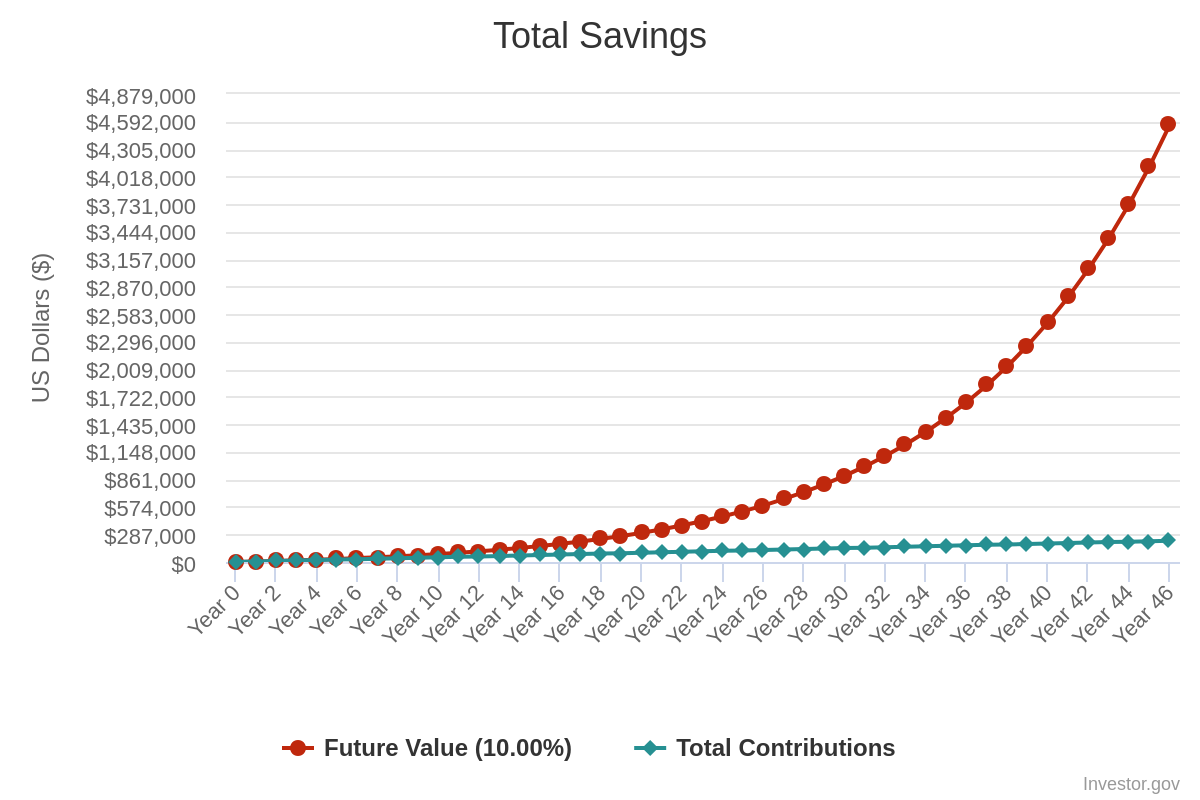

Using his age 24 example, say a first-time investor funded a Roth IRA with $1,000 and purchased shares of an index fund with a historical average return of 10%. With an additional $100 contributed weekly for the next 46 years — at which point they'll be 70 — the total contributed would total $221,800.

However, that retirement account would then be worth $4.55 million without taking dividends into consideration, which most index funds pay quarterly and can be automatically reinvested into positions.

That's the power of compound interest. But that payoff hinges on getting started sooner than later, because delaying that decision means lost opportunity.

As Van Sant puts it, "An investor's best friend is time."

Qualify for up to 10% in FREE silver

Qualify for up to $10k in FREE precious metals*

- Diversify your portfolio by investing in a precious metal IRA or buy gold and silver directly

- Highest price buyback guarantee

- A+ Rating from BBB, AAA Rating from Business Consumers Alliance

Top Ranked Precious Metals Company on the Inc. 5000

Top Ranked Gold Company on the Inc. 5000

- Lowest price guarantee and no buyback fees

- Exclusively recommended by Bill O'Reilly, Rick Harrison, & Others

- A+ Rating from BBB

Price match guarantee and no fees on buybacks

Longest time in business with 27 years of experience

- Recommended by Glenn Beck and Judge Andrew P. Napolitano

- Trusted by over 90,000 customers

- Rated excellent on Truspilot & AAA on Business Consumer Alliance

Provides Guide on Gold IRA Company Scams

Provides Guide on Gold IRA Company Scams

- Augusta representatives available for 1 on 1 sessions

- Recommended by Hall of Fame Quarterback Joe Montana

- Available help from Augusta representatives while creating an account

- Up to 10 years fees reimbursed to your IRA in premium silver coins

Most IRAs Qualify for “No Fee For Life”

Most IRAs Qualify for “No Fee For Life”

- 50 years of collective, combined experience in the markets

- Expert guidance to open a gold IRA account

- Low-Cost Bullion, IRA eligible, and numismatic coins available

- A+ Rating from BBB

More from Money:

Why the Recent Rise in Stock Buybacks Is a Good Sign for Investors